*Updated as of June 2026*

State-mandated retirement plans are rapidly gaining momentum across the U.S., and they are no longer optional for many employers. Each year, more states require businesses above certain employee thresholds, in many cases starting at 5 or more employees and in some states as low as 1 employee, to either offer a qualified retirement plan or enroll employees in a state-facilitated program, with penalties for noncompliance.

What This Means for Businesses

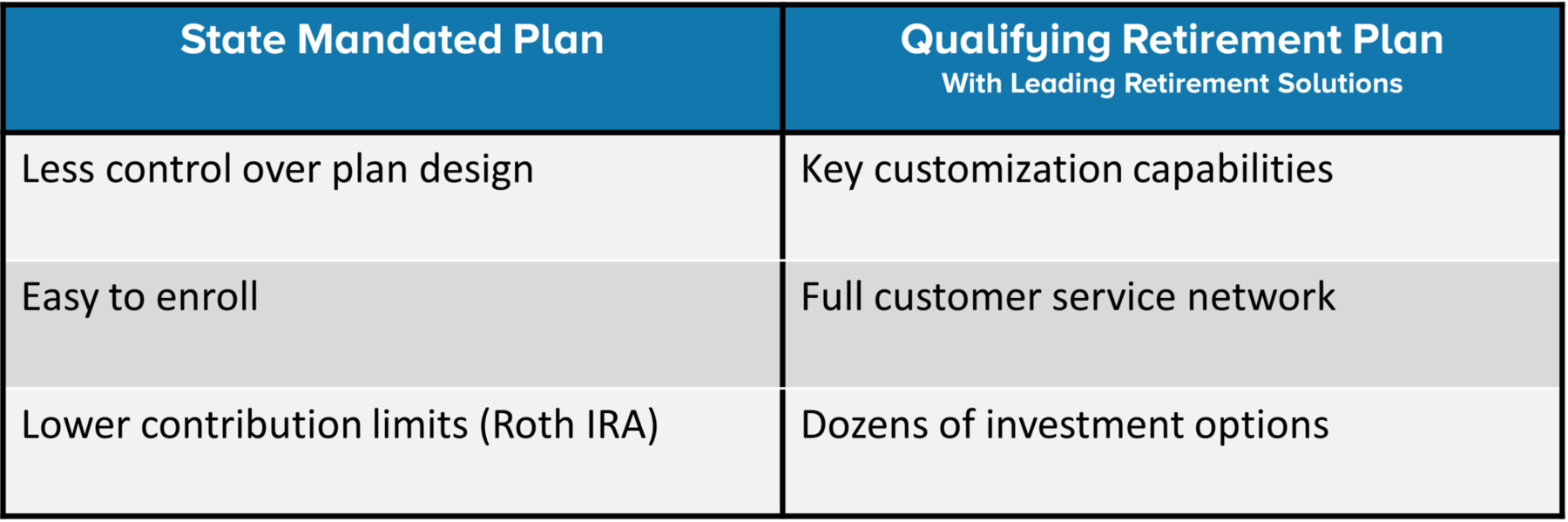

Employers do have options. They can participate in a state program or implement a qualifying retirement plan, such as a 401(k), that meets requirements while offering greater flexibility and added value for both the business and its employees. What began as a handful of pilot programs has evolved into a nationwide push to expand retirement access and increase employer responsibility.

State IRA vs. 401(k) Plans

While state-facilitated IRA programs are designed to help employers meet retirement savings requirements, they offer only a basic savings vehicle funded by employee contributions. In contrast, a 401(k) plan provides higher contribution limits, potential employer matching and profit-sharing contributions, greater plan design flexibility, and provides organizations with an enhanced benefits package. Many employers choose to work with retirement plan providers such as Leading Retirement Solutions (LRS) to implement a compliant 401(k) plan that not only satisfies state mandate requirements but also serves as a valuable tool for employee recruitment, retention, and long-term financial wellness

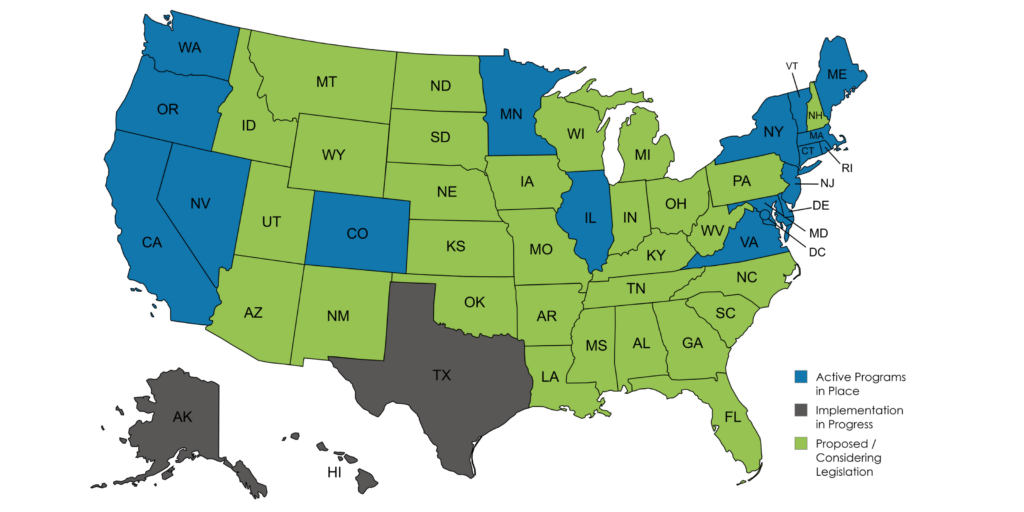

A Record Number of Active State Programs in 2026

As of 2026, 22 states have enacted retirement savings programs, and 17 of those programs are currently open or actively onboarding eligible employers and workers—representing the largest number of active state-facilitated retirement systems to date. This includes 15 Auto-IRA programs across California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Minnesota, Nevada, New Jersey, New York, Oregon, Rhode Island, Vermont, and Virginia, as well as Massachusetts’ nonprofit MEP and Washington’s retirement plan marketplace.

Continued Expansion and Increasing Mandates

Momentum shows no signs of slowing. Additional states have recently enacted new programs (including Utah and Mississippi), bringing the total to 22 states with enacted programs, while others continue advancing legislation or moving from voluntary frameworks to mandatory participation. At the same time, states are tightening requirements and expanding coverage thresholds. For example, New Jersey has lowered its mandate to employers with as few as 10 employees, significantly broadening participation and increasing enforcement exposure. Similarly, Virginia has reduced its threshold from 25 employees to 5 (added), signaling a broader trend toward more inclusive and more enforced mandates.

What’s Inside This Updated State-by-State Guide

This updated guide provides a state-by-state breakdown of each program’s requirements, timelines, penalties, and notable updates, equipping employers with clear insight into current obligations and upcoming changes in this rapidly evolving retirement landscape.

California

California’s Auto-IRA program, CalSavers, provides access to Roth IRAs (default) with the option to recharacterize to Traditional IRAs through payroll deduction for workers whose employers do not sponsor a qualified retirement plan.

Timeline

CalSavers was enacted in 2016.

Employers with 5+ employees were required to comply by 6/30/2022; The mandate was expanded to employers with at least 1+ eligible employee, with a final compliance date of 12/31/2025.

Penalties

Enforcement is $250 per eligible employee after 90 days of noncompliance and an additional $500 per eligible employee if noncompliance continues, with additional annual fines thereafter. Penalties may be reapplied in future years if noncompliance persists, as enforced by the California Franchise Tax Board.

Sources

Georgetown CRI; CalSavers, CA State Treasurer, California Public Law

Colorado

Colorado SecureSavings is an Auto-IRA requiring covered employers without a plan to facilitate payroll-deduction Roth IRAs.

Timeline

Active statewide since 2023; Ongoing compliance: Employers that newly become eligible (e.g., reach 5+ employees and two years in business) are generally required to register by May 15 of the year following eligibility.

Penalties

Guidance commonly references penalties up to $100 per unenrolled eligible employee per year, capped at $5,000.

Sources

Georgetown CRI; Colorado SecureSavings; CO Treasury.

Connecticut

MyCTSavings is fully operational and overseen by the Office of the State Comptroller. In 2025, Connecticut expanded the covered employee definition, authorized Comptroller administered penalties, and aligned certain defaults with federal rules for new participants.

Timeline

Employers with 5+ employees must register by August 31 each year after meeting eligibility.

Penalties

Beginning July 1, 2025, the State Comptroller may impose civil penalties on covered employers that fail to enroll in MyCTSavings or certify a qualifying retirement plan after notice and a cure period. Annual penalties are assessed following a three-notice enforcement process and are set at $500 for employers with 5–24 employees, $1,000 for employers with 25–99 employees, and $1,500 for employers with 100 or more employees, for each year of continued noncompliance.

Sources

Georgetown CRI; MyCTSavings; CT CRSP Board

Delaware

EARNS opened in 2024, offering a state-facilitated Roth IRA to workers without a plan.

Timeline

Employers that employed 5+ covered employees in the prior calendar year, have been in business in Delaware for at least six months, and do not offer a qualifying retirement plan must register for EARNS or certify an exemption upon receiving notice. Registration deadlines are coordinated by the Office of the State Treasurer and program administrator, and newly eligible employers are generally required to comply by October 15 of the applicable year following notification.

Penalties

Non-compliant employers face fines of $250 per unenrolled eligible employee, with a maximum penalty of $5,000 per calendar year.

Sources

Georgetown CRI; EARNS; DE Treasurer.

Hawaii

The Hawaii Retirement Savings Program (HRSP) was enacted in 2022 and amended in 2025 to transition from an opt-in model to automatic enrollment with opt-out. In February 2026, the Hawaii Retirement Savings Board voted to join Connecticut’s MyCTSavings multistate partnership to support and accelerate program implementation.

Timeline

The HRSP is not yet open to employers as of mid-2026, with Board-led implementation and multistate coordination underway.

Penalties

To be determined. Employers should monitor HRSP guidance for final enforcement provisions as the program is implemented.

Sources

Georgetown CRI; Hawaii HRSP

Illinois

Illinois Secure Choice is fully active statewide, requiring covered employers to sponsor a plan or facilitate payroll-deduction IRAs.

Timeline

Ongoing. Private-sector employers that employed 5+ employees in every quarter of the prior calendar year, have been in business for at least two years, and do not offer a qualified retirement plan are required to register for Secure Choice or certify an exemption upon becoming eligible or receiving notice.

Penalties

Frequently cited: $250 per employee in the first noncompliant year; $500 per employee in subsequent years, as enforced by the Illinois Department of Revenue.

Sources

Georgetown CRI; Illinois Secure Choice; IL Treasurer.

Maine

MERIT (Maine Retirement Investment Trust) is the state’s Auto-IRA for employers with 5+ covered employees and two years of operations, unless a qualified plan is offered.

Timeline

Opened January 2024; newly eligible employers register by June 30 following the year they meet thresholds.

Penalties

Scheduled enforcement escalates: $20 per employee (7/1/2025–6/30/2026), $50 (7/1/2026–6/30/2027), $100 on/after 7/1/2027. (Earlier periods included $10.)

Sources

Georgetown CRI; MERIT; MERIT Board

Maryland

MarylandSaves launched in 2022 and facilitates Roth IRAs; the state also offers an SDAT filing fee waiver for registered employers (or those with a qualifying plan).

Timeline

Employers with 1+ employees, at least two years of operations, and an automated payroll system, generally register by December 31 annually (or certify exemption).

Penalties

No penalties currently; the incentive is the $300 SDAT annual report fee waiver for compliant employers.

Sources

Georgetown CRI; MarylandSaves; MD administrative site

Massachusetts (Voluntary – Nonprofits)

The state-facilitated multiple employer 401(k) plan known as the CORE Plan remains voluntary and, as of 2025, expanded employer eligibility to include nonprofits with up to 100 employees.

Timeline

Available now to eligible nonprofits; nonprofits opt in at any time. Once an employer adopts the plan, eligible employees receive a 60-day notice period and are automatically enrolled unless they opt out.

Penalties

None (voluntary program).

Sources

Georgetown CRI; Mass.gov CORE Plan

Minnesota

Minnesota Secure Choice is one of the newest state-facilitated Auto-IRA programs. The program becomes operational in January 2026, with phased mandatory registration requirements based on employer size.

Timeline

Soft launch: January 19–March 30, 2026. Registration deadlines are phased by employer size: 100+ employees – June 30, 2026; 50–99 – December 31, 2026; 25–49 – June 30, 2027; 10–24 – December 31, 2027; 5–9 – June 30, 2028.

Penalties

Employers receive notices and cure periods before penalties are imposed. The Minnesota Secure Choice Retirement Board currently publishes a graduated penalty schedule beginning at $100 per employee (maximum $4,000), increasing to $200 per employee (maximum $6,000), then $300 per employee, and ultimately $500 per employee with no maximum cap for ongoing noncompliance.

Sources

Georgetown CRI; MN SCRB.

Nevada

Nevada’s Auto-IRA, NEST (Nevada Employee Savings Trust), is administered by the Nevada Treasury and is operational and available statewide to eligible employers and workers.

Timeline

Employers with 6+ employees and 36 months of operations are generally covered; onboarding and registrations are coordinated by Treasury and the program administrator. Covered employers were initially required to register or certify an exemption by September 1, 2025.

Penalties

While Nevada law authorizes enforcement, specific penalties for employer noncompliance have not yet been finalized. Employers should continue to monitor NEST and State Treasurer guidance for future enforcement details.

Sources

Georgetown CRI; NEST; NV Treasurer.

New Jersey

RetireReady NJ is New Jersey’s state-administered Auto-IRA program. The state has amended its law to reduce the employer threshold from 25 to 10 employees (implementation schedule forthcoming in 2026).

Timeline

Initial rollouts completed in 2024 for 25+ employers; additional waves are expected as the threshold lowers.

Penalties

Enforcement provisions apply under the statute; employers should monitor RetireReady NJ for updated schedules and amounts as the threshold change is implemented.

Sources

Georgetown CRI; RetireReady NJ.

New Mexico (Voluntary / Inactive)

New Mexico’s “Work & $ave” was established as a voluntary marketplace/IRA concept, but the program is inactive as of 2025 per the State Treasurer.

Timeline

Implementation has been delayed; no active employer registration at this time.

Penalties

None (inactive/voluntary).

Sources

Georgetown CRI; NM State Treasurer.

New York

The New York Secure Choice Auto-IRA is launching statewide under the oversight of the Secure Choice Board.

Timeline

Employer registration deadlines: 30+ employees (Mar 18, 2026), 15–29 (May 15, 2026), 10–14 (Jul 15, 2026); employers must register within the assigned wave or certify exemption.

Penalties

Enforcement and penalty details flow from state statute and Board guidance; employers should review Board resources as program phases progress. Based on current Secure Choice Board–aligned guidance, penalties are expected to follow structures similar to other Auto?IRA states.

Sources

Georgetown CRI; NY Secure Choice (program + Board).

Oregon

OregonSaves, launched in 2017, was the nation’s first state-facilitated Auto-IRA program and is now fully implemented statewide. All Oregon employers that do not offer a qualified retirement plan are required to register and facilitate OregonSaves or certify an exemption.

Timeline

The program is ongoing, with rolling onboarding for newly established or newly covered employers.

Penalties

Oregon law authorizes civil penalties for employer noncompliance. Employers that fail to register, certify exemption, or facilitate the program may be subject to a penalty of $100 per eligible employee, capped at $5,000 per calendar year, enforced through the Oregon Bureau of Labor and Industries.

Sources

Georgetown CRI; OregonSaves; Oregon Treasury (Board).

Rhode Island

RISavers launched Oct 21, 2025, providing an Auto-IRA for workers at employers without a plan. The program is overseen by the Rhode Island Office of the General Treasurer.

Timeline

Phased compliance: >100 employees by Oct 15, 2026; 50–99 by Oct 15, 2027; 5–49 by Oct 15, 2028. Employers receive a noncompliance notice before further action.

Penalties

Upon issuance of a noncompliance notice, employers that fail to comply within 30 days may be subject to a civil penalty of $250 per eligible employee, as authorized under Rhode Island General Laws §352315. Penalties are enforced by the Office of the General Treasurer with assistance from the Department of Labor and Training.

Sources

Georgetown CRI; RI Treasurer press releases (launch + memo); RISavers;

Vermont

Vermont Saves is open and requires employers with 2+ employees that have been in business for at least 2 years to register unless they offer a qualified retirement plan. The employee threshold was expanded from 5 employees to 2 employees in 2026.

Timeline

Initial employer registration deadline was February 2025; Employers that become newly covered—such as by reaching five+ employees or exceeding 2 years in business—continue to onboard on a rolling basis and must register or certify exemption within the state-specified timeframe.

Penalties

Civil penalties through Treasurer-adopted rules, with a phased escalation over time. Maximum penalties have been set at up to $10 per employee prior to October 1, 2025; up to $20 per employee from October 1, 2025, through September 30, 2026; and up to $75 per employee on or after October 1, 2026. Employers should consult the Vermont Saves program site and the Treasurer’s guidance for current enforcement details and applicability.

Sources

Georgetown CRI; Vermont Saves; VT Treasurer.

Virginia

RetirePath Virginia is an Auto-IRA launched in 2023, administered by Commonwealth Savers (formerly Virginia529). Employer threshold reduced from 25 employees to 5 employees effective July 1, 2026.

Timeline

Ongoing registration for covered employers; employees are auto-enrolled with a 30 day decision window to customize or opt out.

Penalties

Employers that fail to register or certify an exemption after receiving notice may be subject to penalties of up to $200 per eligible employee per year, as applied pursuant to program guidance.

Sources

Georgetown CRI; RetirePath Virginia.

Washington (Voluntary)

Washington operates the voluntary Retirement Marketplace, which lists verified private retirement plans for small employers and individuals. The state also enacted Washington Saves (Auto-IRA) with a planned launch in 2027.

Timeline

Marketplace is active now; the statewide Auto-IRA program timeline targets 2027 for launch (watch for board/agency updates).

Penalties

None for the Marketplace (voluntary). Auto-IRA enforcement details will be issued closer to launch.

Sources

Georgetown CRI; WA Retirement Marketplace.

Footnotes — Administrative / Board Links (for deeper policy/legislative detail)

- California: State Treasurer’s CalSavers page — https://www.treasurer.ca.gov/calsavers/

- Colorado: State Treasury program — https://treasury.colorado.gov/programs/retirement-savings

- Connecticut (OSC): CRSP/Board hub — https://osc.ct.gov/crsp/

- Delaware: Treasurer’s EARNS page — https://treasurer.delaware.gov/earns/

- Hawaii: HRSP board/implementation — https://labor.hawaii.gov/hrsp/

- Illinois: Treasurer hub — https://illinoistreasurer.gov/home/individuals/secure-choice/

- Maine: MERIT board site — https://meritsaves.org

- Maryland: MarylandSaves organization — https://www.marylandsaves.org/

- Massachusetts CORE (Treasurer): https://www.mass.gov/core-plan-for-nonprofits

- Minnesota: Secure Choice Board — https://mn.gov/scrb/

- Nevada: Treasury NEST hub — https://www.nevadatreasurer.gov/NEST/

- New Jersey: RetireReady NJ (Treasury) — https://nj.gov/treasury/securechoiceprogram/employers/index.shtml

- New Mexico: Work & $ave status — https://www.nmsto.gov/work-and-save

- New York: Secure Choice Board — https://www.securechoice.ny.gov/

- Oregon: Retirement Savings Board — https://www.oregon.gov/treasury/Upward-Oregon/Pages/Oregon-Retirement-Savings-Board.aspx

- Rhode Island: Treasurer’s RISavers launch & memo — https://treasury.ri.gov/press-releases/treasurer-diossa-celebrates-launch-risavers ; https://treasury.ri.gov/press-releases/important-information-regarding-risavers-program

- Vermont: Treasurer’s Vermont Saves — https://www.vermonttreasurer.gov/economic-empowerment-division/vermont-saves

- Virginia: RetirePath Virginia — https://www.retirepathva.com/

- Washington: DFI Marketplace page — https://dfi.wa.gov/small-business-retirement-marketplace

National Reference

- Georgetown Center for Retirement Initiatives – 2026 States Page (open programs, legislative trends): https://cri.georgetown.edu/states/

A Retirement Plan Built for Your Business

If your state has not instituted a retirement plan, or your looking for a plan that is designed around your business needs, we’ve got the solution:

Connect with us on Facebook, LinkedIn, and Twitter!

For tips and information regarding retirement plans, contact us.